Opinion: How to bear this market

by Donald Gould

Stocks worldwide have declined steadily from their all-time highs reached at the start of 2022. The benchmark S&P 500 US stock index recently exceeded the 20% decline from peak that (arbitrarily) defines a bear market. Adding to investor woes, bonds have not provided their usual portfolio cushion this year. The Bloomberg US Aggregate bond index fell about 10% in the first half of 2022.

Resurgent inflation

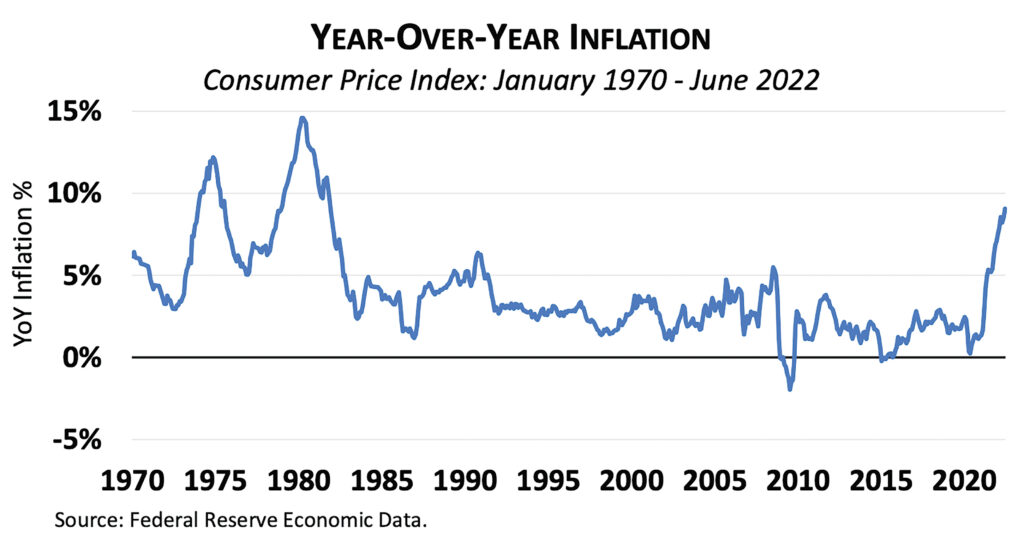

Resurgent inflation is the proximate cause of both markets’ swoon this year. After ranging between 0% and 4% for the past 30 years, the Consumer Price Index clocked an 9.1% jump in the year ended June 30. High energy and food prices, exacerbated by the war in Ukraine, are significant contributors, as are consumer catch-up spending and a still tight labor market coming out of the pandemic. The inflation spike triggered a row of market dominoes.

First, the Federal Reserve is aggressively raising short-term interest rates, seeking to tamp down demand and moderate further price hikes. Interest rates on all bond maturities are way above where they began the year. Short-term rates (for example, the three-month US T-bill), which are most directly affected by Fed policy, jumped from a microscopic 0.06% at the beginning of the year to 1.72% on June 30. Meanwhile, the benchmark 10-year Treasury yield nearly doubled from 1.52% at year-end to 2.98%. When market interest rates rise, the price of existing bonds must fall to keep their yields competitive with yields on new bonds.

Second, most see rising odds of economic recession in the next year. Higher interest rates dampen growth across the economy, and spiking prices for staple items like gasoline and groceries leave less in the household budget for other spending.

Finally, recession brings lower corporate earnings, while higher interest rates make bonds more competitive with stocks. These are double body blows for the stock market.

Perils of anchoring

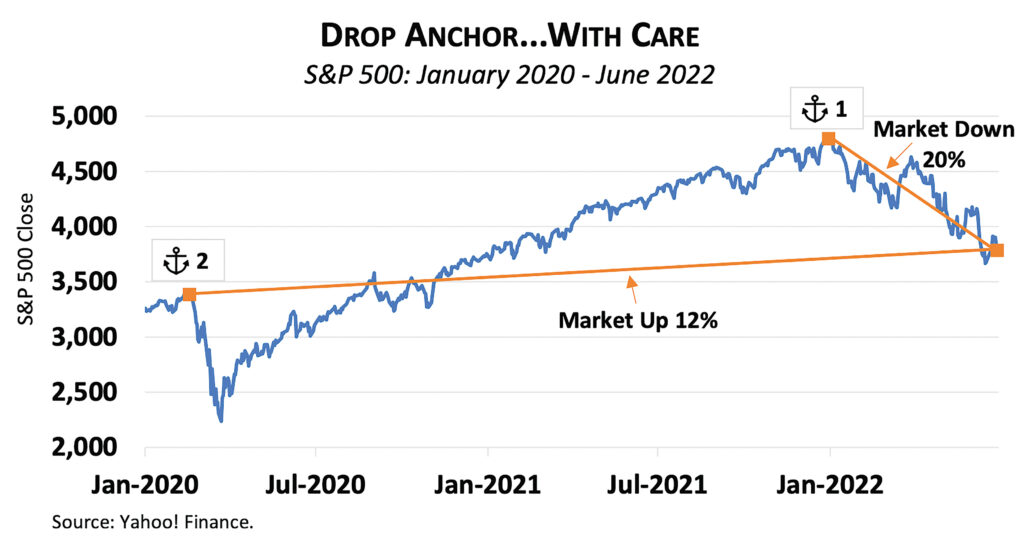

Seeing our portfolio values shrink is unpleasant, even if only on paper. It is human nature to mentally anchor our assets to their maximum historical price, whether that’s the highest value your home reached on Zillow or the biggest number shown on a monthly brokerage statement.

It’s easy to think, “If only I’d sold at that high water mark, I’d be better off now.”

Perhaps true, but consider this: we only know a high-water mark with the benefit of hindsight. And it is impossible for everyone to sell (at a high-water mark or any other time) because for every seller there must be a buyer. In other words, selling at a peak assumes you’ve figured out something the rest of the market has not — a tempting line of thinking that’s generally hazardous to your financial wellbeing.

Selling last December (Anchor 1 in the accompanying chart) would have entailed substantial tax liability for most investors, never to be regained. As bad, it would leave you sitting in cash wondering when to get back in. Market bottoms, like tops, are only known with hindsight and often occur when pessimism seems to be running highest. In our experience, investors who bail out amid a bear market rarely reenter at a level below their earlier sale price.

Consolation and perspective

One way to combat regret after a market decline is simply to relocate your anchor. For example, if instead of comparing your assets today to their value at year-end 2021, look to February 19, 2020 (Anchor 2 in the chart), at that time also an all-time high for the S&P 500. Since then, the US stock market is up nearly 12%. Considering that the period included a pandemic, a land war in Europe, and unprecedented political turmoil, 12% could be viewed as a surprisingly good outcome.

Many rightly worry that recession is coming soon or perhaps already here. But from a market perspective, that news is already baked into today’s prices and probably explains much of the recent decline. No one has a crystal ball to foretell where the market will go next, but the odds still favor buying (or holding) stocks after significant market declines.

Looking at post-World War II data, following a 20% decline like we’ve had this year, the S&P 500 finished higher at the end of the subsequent 12-month period about 64% of the time — less than the 79% of calendar years that were positive, but still almost two-in-three odds of coming out ahead. Three years out, the market ended higher 90% of the time. (Source: FactSet, Bloomberg, as of 6/16/22.) Consumer sentiment recently reached record lows, thanks to high inflation, but that has often been an indicator of better stock market performance ahead.

Bottom line: in stormy seas, it’s usually best to take a Dramamine and lash yourself to the mast rather than jumping overboard.

Don Gould is president and chief investment officer of Gould Asset Management of Claremont.

0 Comments